Kenya built the most advanced EV market in East Africa. Then it proposed a tax that makes Rwanda look smarter by the day.

The number that matters this week is not a funding round. It is a parliamentary deadline: July 1, 2026. That is when Kenya's Finance Bill 2026 — currently before the National Assembly, public submissions still open — is scheduled to take effect if passed. And buried inside it is a clause that has BasiGo, Ampersand, Spiro, and every electric bus operator in the country quietly revising their unit economics.

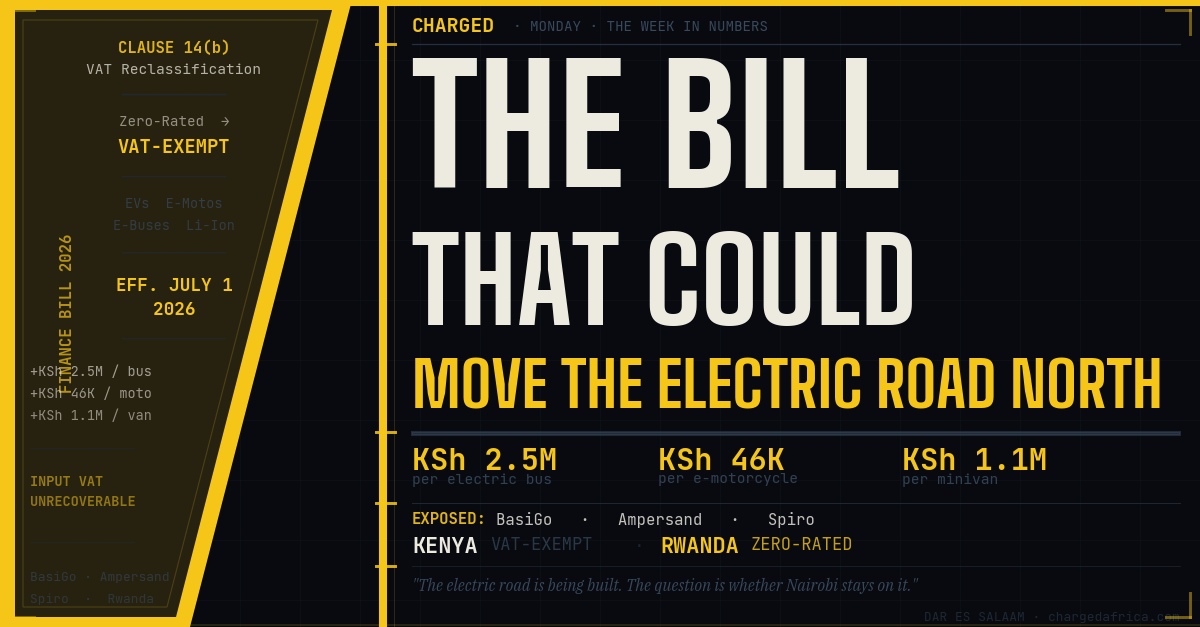

The clause? Moving electric vehicles, electric motorcycles, electric buses, lithium-ion batteries, and solar batteries from zero-rated to VAT-exempt status.

Most coverage has called this "a VAT proposal on EVs" and left it there. That framing misses what is actually happening.

THE NUMBER MOST COVERAGE IS GETTING WRONG

Zero-rated and VAT-exempt are not the same thing. This is the detail that separates the operators who understand their exposure from those who will discover it in a quarterly report.

When a product is zero-rated, the importer or assembler charges 0% VAT to the customer — AND can reclaim the VAT paid on all inputs: components, shipping, services, materials. The Finance Act 2025, passed less than twelve months ago, gave Kenya's EV sector exactly this: zero-rated status for electric buses, motorcycles, and lithium-ion batteries.

When a product is VAT-exempt, the customer still does not pay VAT. But the importer or assembler loses the right to claim back the VAT on inputs. Every kilowatt-hour of battery cell imported. Every CKD component assembled in Mombasa. Every delivery service. That input VAT stacks up inside the cost base and cannot be recovered.

The difference, for a single electric bus, is a KSh 2.5 million increase in landed cost. For an electric motorcycle: KSh 46,000 per unit. For an electric minivan: KSh 1.1 million.

BasiGo MD Moses Nderitu called it "a shocking proposal, given the support we have had from the government." That is not a public relations statement. It is a balance sheet observation.

WHO IS EXPOSED, AND HOW MUCH

BasiGo is the operator most directly in the crosshairs. The company launched local assembly of its Ma3e electric vans at Associated Vehicle Assemblers in Mombasa in April 2026 — two months before the Finance Bill was tabled. It has more than 1,200 reservations for additional units and is targeting 1,000 buses on Kenyan roads by 2027. Under the zero-to-exempt reclassification, the CKD kits being assembled in Mombasa immediately attract unrecoverable input VAT. Local assembly, which was supposed to lower costs, now increases them. The industry study that found "all or almost all inputs for EVs are imported" was written as a risk flag. The Finance Bill has converted it into a cost reality.

Ampersand operates in both Rwanda and Kenya. Its Rwanda operations — battery swaps, fleet financing, its BYD-backed target of 40,000 e-motorcycles by end-2026 — are untouched. Rwanda offers 0% import duty and VAT waivers on locally assembled EVs. The Kenyan arm of the same company, meanwhile, would absorb an additional KSh 46,000 per motorcycle in input VAT if the bill passes. The geographic hedge Ampersand built by being Rwanda-first looks less like caution and more like prescience.

Spiro, which raised $215 million in June 2026 and now operates 100,000 electric motorcycles and 2,500+ battery swap stations across multiple African markets, has Kenya as one of its expansion markets. It has not issued a public statement on the Finance Bill. It does not need to — the math is the same for every operator importing lithium-ion batteries at scale.

THE EAST AFRICA COMPARISON

This is where the policy story becomes a capital allocation story.

| Market | EV Import Duty | VAT on EVs | Battery Status |

|---|---|---|---|

| Kenya | 0% | Exempt (proposed) | Zero-rated → Exempt |

| Rwanda | 0% | 0% (waived) | Zero-rated, input VAT recoverable |

| Uganda | Exemptions (partial) | Mixed | Evolving |

| Tanzania | Excise duty applies | Exempt | Higher than ICE in some categories |

Rwanda is the outlier — deliberately so. Its EV policy treats the sector as industrial infrastructure, not a consumer discretionary import. VAT waivers on locally assembled EVs, zero import duty on equipment and charging infrastructure, and a regulatory environment that Ampersand has used to build the largest e-motorcycle battery swap network in East Africa.

If the Kenya Finance Bill passes as written, it creates a direct arbitrage: the same electric motorcycle costs KSh 46,000 more to put on a Nairobi road than on a Kigali road. At scale — Spiro's 100,000 bikes, Ampersand's 40,000 target — that differential is not noise. It is a strategic decision about where to deploy the next fleet.

THREE THINGS TO WATCH BEFORE JULY 1

1. Whether the industry lobbying moves the clause. Public participation closes before July 1. The Kenya Association of Manufacturers and the e-mobility operators have standing to submit memoranda. Bowmans Law has already published a detailed Finance Bill analysis flagging the EV reclassification. The window is narrow.

2. BasiGo's Mombasa assembly economics in Q3. The company started CKD assembly in April. If the bill passes with the exemption clause intact, BasiGo will be the clearest case study of what happens to local EV industrialisation under input VAT exposure. Watch for any pricing adjustment announcement or order book update.

3. Whether Rwanda accelerates operator incentives. If Kenya passes the bill, every East Africa e-mobility operator with a cross-border footprint has a reason to weight capital toward Rwanda and away from Kenya. Rwanda's government has been deliberate about this positioning. A Kenyan policy mistake is, from Kigali's perspective, a competitive opportunity.

THE CHARGED READ

Kenya's 2024 Finance Bill protests ended with Parliament being stormed and the bill being withdrawn. That episode reset the terms of every fiscal conversation in the country: no tax proposal is assumed to pass until it passes.

What is different in 2026 is that the EV sector now has skin in the game. BasiGo is assembling buses in Mombasa. Spiro has swap stations in Nairobi. Ampersand has riders on Kenyan roads. These are not lobbying positions on paper. They are deployed capital that will be immediately mispriced if the exemption clause survives to July 1.

Kenya built the strongest EV policy environment in East Africa in 2025, faster than anyone expected. It is now proposing to unwind it, faster than anyone planned for.

The electric road is being built. The question is whether Nairobi stays on it.

CHARGED is published every Monday (The Week in Numbers) and Thursday (Deep Signal). Dar es Salaam.