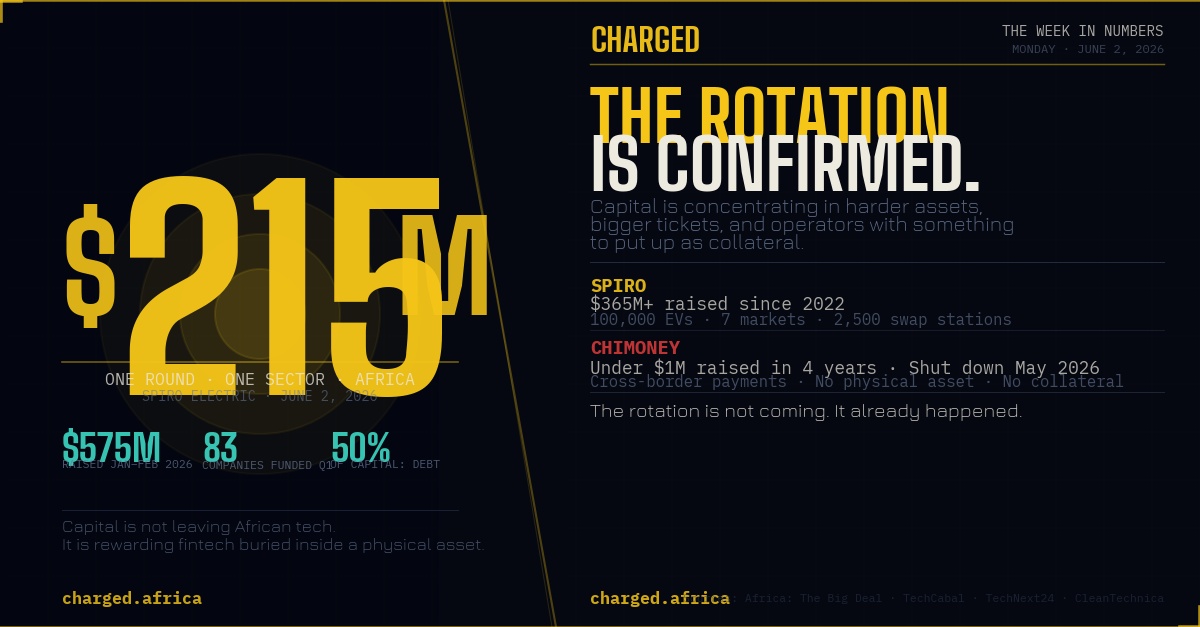

$215 million. One company. One sector. Africa's largest-ever clean mobility investment, announced this morning by Spiro — and it isn't even the most important number in today's edition.

The number that matters more is this one: 83.

That's how many African startups raised at least $100,000 in Q1 2026, according to Africa: The Big Deal. Down from 130 in Q1 2025. The total capital raised went up — from $470M to over $700M. The number of companies getting funded went down by 36%.

That is the story of African tech in 2026. Not a boom. A rotation. Capital is concentrating — in bigger tickets, in harder assets, in companies that have cracked unit economics and can take institutional debt. The middle layer — the small-ticket fintech building API infrastructure on borrowed runway — is quietly running out of road.

Chimoney proved it last month. Four years. Forty-one currencies. Under $1 million raised. On May 12, the Nigerian-Canadian fintech shut down.

The same week, MAX closed $8 million in debt from Triple Jump — its first international institutional lender. Different outcome. Same sector label: fintech. The difference isn't the label. It's whether there's a physical asset underneath the product.

THE NUMBERS THAT DEFINE THE WEEK

$575M — total raised by African startups across January and February 2026. The fastest opening 60 days on record, surpassing the same period in 2025 by more than $100M. This is not a blip.

$215M — Spiro's equity round announced this morning, backed by Impact Fund Denmark and Equitane. Spiro has now raised more money in the last eight months than most active African fintechs have raised in their entire existence. The company operates 100,000 electric motorcycles and 2,500 smart-swap stations across seven markets: Kenya, Uganda, Rwanda, Nigeria, Benin, Togo, and Cameroon. Manufacturing plants in Kenya, Rwanda, and Uganda. A battery recycling facility in Nigeria. This is no longer a startup operating at scale. This is infrastructure.

$161M — what e-mobility startups raised across Q1 2026, across 10 deals. Against fintech's $208M across 20 deals. Fintech raised more. In twice as many deals. The average e-mobility ticket: $16.1M. The average fintech ticket: $10.4M. The money is concentrating where the asset base is hardest.

~50% — share of Q1 2026 capital that arrived as debt, not equity. This is the structural shift that most coverage misses. When Afreximbank writes a $50M debt cheque to Spiro in February, that's not venture capital looking for a 10x return on a consumer app. That's a development finance institution treating battery-swap infrastructure the same way it used to treat telecom towers and toll roads. The instrument is the signal.

THE DEAL MAP THIS WEEK

Spiro — $215M equity (June 2026): Benin-headquartered, now operating across seven African markets with 100,000 EVs deployed. Lead investors: Impact Fund Denmark + Equitane. This follows a $50M debt raise in February and a $100M equity round in October 2025. Total raised since 2022: north of $365M. The cap structure conversation for Spiro is now about strategic consolidation or public markets — not survival.

GoCab — $45M (February 2026): Côte d'Ivoire-headquartered mobility fintech expanding electric vehicle financing across Francophone West Africa. The biggest February deal outside of Spiro. A signal that the Francophone market — historically underrepresented in African tech coverage — is finding its capital moment.

Zeno — $25M (Q1 2026, Kenya): East Africa's quiet contender in electric two-wheeler financing. Fleet expansion in Kenya is the primary use of funds. Nairobi's boda boda market remains the most competitive testing ground for EV unit economics on the continent.

MAX — $24M round + $8M debt from Triple Jump (Q1 + May 2026): Nigeria's electric motorcycle platform hit profitability before its latest raise — a sequencing that most African mobility operators have not managed. Triple Jump's participation signals that the international institutional debt market for African EV is opening, not just the DFI window.

WHAT THE CHIMONEY STORY TELLS US

Uchi Uchibeke, Chimoney's founder, wrote one of the most honest post-mortems in African tech history when he announced the shutdown. "The product worked. It was distribution. I spent too much time building and not enough time making sure people knew what we built."

He's right about the product. But there's a structural reality beneath the distribution problem: cross-border payment infrastructure, built on API rails, without a proprietary physical asset, is extraordinarily hard to finance in this market. You cannot put API endpoints up as collateral. You cannot take debt against a developer dashboard. The fintech middle layer — well-built, technically sophisticated, capital-light — is exactly what DFIs and institutional lenders cannot fund at scale.

What they can fund: 100,000 electric motorcycles generating 30 million swap transactions. Batteries with a residual value. Swap stations with a grid connection. Riders with a repayment history.

The capital is not abandoning fintech. It is rewarding fintech that has buried itself inside a physical asset.

THREE THINGS TO WATCH THIS WEEK

1. Spiro's $215M deployment geography. The announcement references expansion but not specific new market entry. Tanzania is the obvious candidate — it connects Kenya, Uganda, and Rwanda into a single East African EV corridor. Watch for a Dar es Salaam announcement.

2. The DFI pipeline for Q2. Afreximbank, IFC, Proparco, and the Africa Go Green Fund all deployed capital into e-mobility in Q1. Q2 deal closings typically announce 6–8 weeks after signing. The pipeline is active.

3. Kenya's Finance Bill. Parliament resumes deliberations this week. The proposed 16% VAT on electric vehicles, lithium batteries, and e-bikes is still on the table. If it passes, the operators who just raised on Kenyan unit economics will need to remodel. If it fails, the East Africa corridor is clear for aggressive deployment. This is the most consequential policy vote for the sector in 2026.

THE CHARGED READ

Two things are true simultaneously: African tech is raising more capital than ever before, and fewer companies are getting funded than at any point in the last three years.

The operators and investors who understand what that means — that the middle is being selectively abandoned, not the sector — are positioned for the next 18 months. The ones still pitching payment infrastructure without a physical asset anchoring the unit economics are in the hardest fundraising environment of the decade.

$215M for one EV company. Under $1M for four years of cross-border payments work. The rotation is not coming. It already happened.

CHARGED is published every Monday (The Week in Numbers) and Thursday (Deep Signal). Dar es Salaam.