BCG published a report this month that every African fintech founder should read, not because it tells you something new, but because it finally says in a $10 billion consulting voice what the data has been whispering for three years: the payment wave is over. The credit wave has begun. Africa's fintech revenues could grow from roughly $10 billion today to more than $65 billion by 2030 and the engine of that growth will be embedded finance and digital lending, not another cross-border remittance API.

Here is the part BCG does not fully say: the companies best positioned to capture that credit wave are not building credit products. They are building battery swap stations.

That is the thesis. Let me explain it.

THE MECHANISM

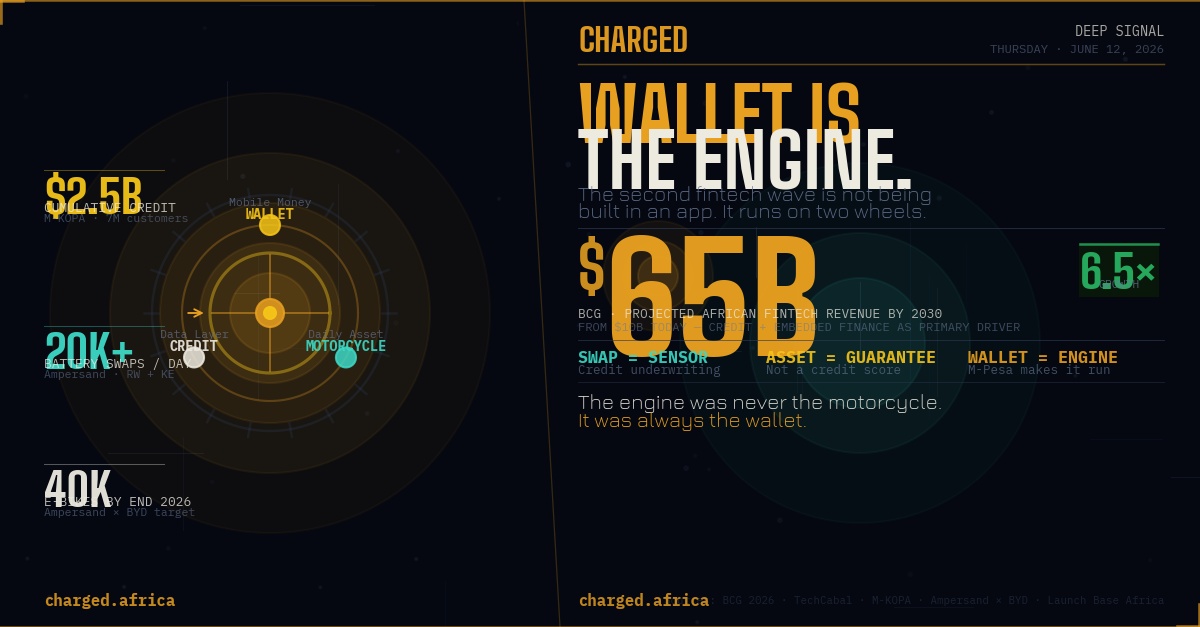

M-KOPA has deployed $2.5 billion in cumulative credit to more than seven million customers across Kenya, Uganda, Nigeria, Ghana, and South Africa. In April 2026 alone, the company unlocked $22.5 million in South Africa a market where it launched only recently. It has also deployed ₦231 billion (roughly $170 million) in Nigeria to over one million customers.

Most coverage frames M-KOPA as a smartphone financier that added e-bikes. That framing misses the architecture. M-KOPA is a credit infrastructure company that uses physical assets — solar panels, smartphones, electric motorcycles as the mechanism for underwriting. The product changes. The mechanism does not.

Here is how the mechanism works.

A rider in Mombasa picks up an M-KOPA electric motorcycle. She pays a small deposit. Every day she rides, she earns. Every day she earns, she repays in increments calibrated to her income. The repayment rails are M-Pesa. The underwriting model is not a credit score. It is the pattern of daily necessity. She needs the motorcycle to earn. She earns to repay. The repayment loop is as close to guaranteed as unsecured lending gets in any market.

The wallet mobile money is the engine. The motorcycle is the chassis. Without M-Pesa and its equivalents, none of this is possible. The entire model depends on the ability to collect KES 150 a day from 100,000 riders simultaneously. That infrastructure did not exist in Africa fifteen years ago. It does now. And the companies who understood what it enabled are the ones being funded.

THE SWAP IS THE SENSOR

Ampersand does more than 20,000 battery swaps per day across Rwanda and Kenya. Each swap is, functionally, a credit event. The rider arrives at a station, exchanges a depleted battery for a charged one, and the transaction is logged. That log becomes behavioral data: how often does she ride, at what times, on which routes, with what frequency? After 90 days of swaps, Ampersand knows more about this rider's income pattern than any Rwandan commercial bank.

That data is the foundation for the next product a cash loan, a health insurance policy, a smartphone purchase, a savings account. This is why the BYD partnership matters beyond the headline. Ampersand and BYD have agreed to scale to 40,000 electric motorcycles by end of 2026. Every additional motorcycle is not just a transport asset. It is a new data collection node in a credit underwriting network that will, in three years, be worth more than the hardware it runs on.

The swap station is not an energy asset. It is a sensor. The motorcycle is not a transport product. It is a credit instrument. Once you see the architecture this way, the BCG projection of a $65 billion African fintech market by 2030 stops being an aspiration and starts being an underestimate.

WHAT WATU UNDERSTOOD FIRST

Watu Africa has been making this argument with its balance sheet since 2015. The company has disbursed more than two million loans across eight Sub-Saharan African markets. It is now targeting $340 million in revenue in 2026 and has flagged expansion into Latin America — a signal that the model, refined in East Africa, is now considered exportable.

Forty percent of Watu's loan book is EV asset financing. That is not incidental. It is the thesis, expressed in portfolio composition. Watu's CFO Steve Onyango told CFO East Africa that the EV transition is, for Watu, a credit opportunity: the e-bike has lower maintenance costs than a petrol motorcycle, which means higher net income for the rider, which means better repayment behavior, which means a better loan book. The clean energy argument and the credit argument are the same argument.

When you start seeing these companies through a credit lens rather than a mobility lens, the funding story becomes legible. Watu, M-KOPA, Ampersand, and GoCab are not raising money to sell more motorcycles. They are raising money to acquire more credit customers at the lowest possible cost — and they have found that strapping a credit product to a daily-necessity physical asset is the cheapest, most reliable customer acquisition channel in markets where formal credit histories do not exist.

THE BCG GAP

BCG's report projects that digital lending and embedded finance will contribute up to half of Africa's fintech revenues by 2030. What the report underweights is the physical layer. The companies that win the African credit wave will not win purely through algorithm. They will win through asset-backed data moats proprietary behavioral datasets built on millions of daily transactions across physical goods that their customers cannot afford to stop using.

This is not the credit model that European fintechs are building. It is something different. It is credit designed around necessity, not preference. A rider in Nairobi does not borrow money to buy a motorcycle because she wants one. She borrows because her family eats based on what she earns that day. That necessity is the repayment guarantee that no credit scoring model can replicate.

The second fintech wave in Africa will be built on this. The question is not whether it will happen. The question is whether the companies building it will be the ones we expect.

M-KOPA, Watu, and Ampersand have a two-to-five-year head start. The wallet is already the engine. The rest of the sector is still looking for the ignition.

THE CHARGED READ

I have watched this model work from closer than most. The question operators always face and the one DFI debt investors now use as a primary filter is not "what is your LTV?" It is "what happens if the borrower stops repaying?" For an API-only fintech, the answer is expensive legal recovery and a bad debt write-off. For Watu or M-KOPA, the answer is simpler: we repossess the motorcycle. The physical asset is the guarantee. The credit product is built inside it.

The second wave will be won by operators who figured out that Africa's informal sector does not need a smarter credit scoring algorithm. It needs a daily necessity attached to a daily payment and a wallet that can move KES 150 at 6am without a bank.

The engine was never the motorcycle. It was always the wallet.

CHARGED publishes every Monday (The Week in Numbers) and Thursday (Deep Signal). Dar es Salaam.