DFIs are not writing $50M+ cheques into African e-mobility because they care about the climate. They're doing it because the numbers finally work and they got there before anyone else.

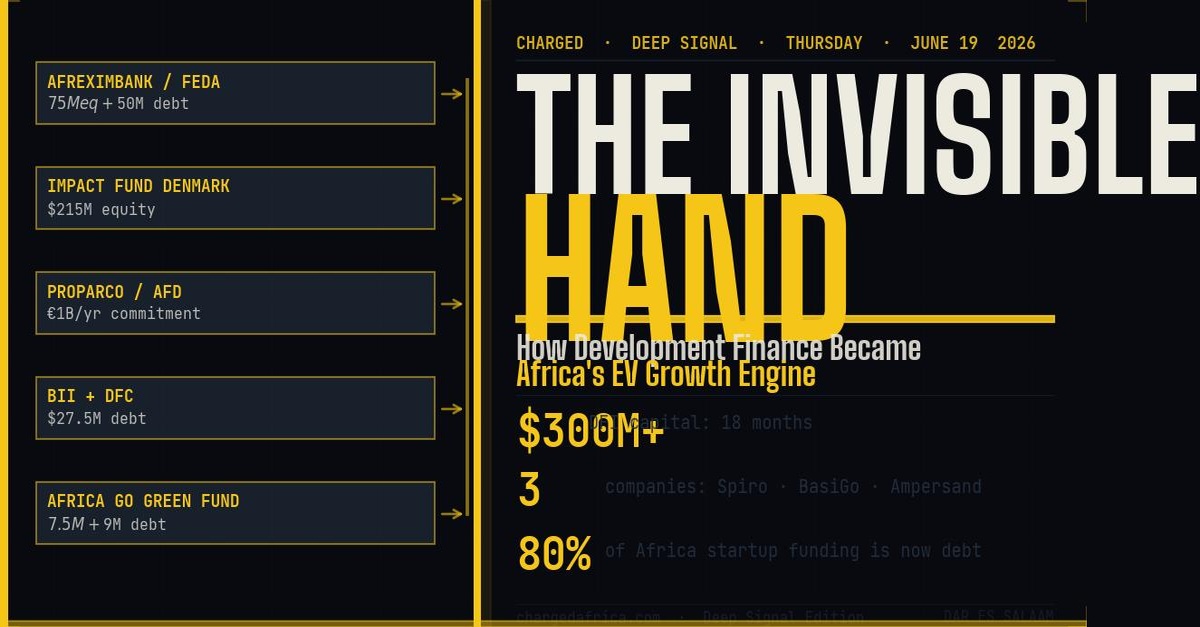

Here is a number that does not appear in any single press release, because it was never meant to be read as one story: in the eighteen months between October 2025 and June 2026, development finance institutions and their affiliated funds committed more than $300 million to just three African e-mobility companies Spiro, BasiGo, and Ampersand.

Not venture capital. Not strategic corporate investment. Structured, patient, asset-backed development finance.

The DFI that led Spiro's $100 million equity round in October 2025 was Afreximbank's Fund for Export Development in Africa (FEDA) the impact investment arm of a multilateral continental bank. Four months later, Spiro returned for a $50 million debt facility from Afreximbank, Nithio, and the Africa Go Green Fund. In June 2026, Impact Fund Denmark the Danish state's development finance vehicle — anchored the $215 million equity round that pushed Spiro's total capital raised past $343 million since 2022.

BasiGo's table tells the same story. The Nairobi-based electric bus company drew $27.5 million in debt from British International Investment (BII) and the U.S. International Development Finance Corporation (DFC), followed by an undisclosed equity stake from Proparco the private-sector arm of France's Agence Française de Développement in November 2025, as part of AFD's commitment to deploy roughly €1 billion per year into low-carbon transport worldwide.

Ampersand, the Rwanda-headquartered battery swap operator, drew a $7.5 million senior debt facility from the Africa Go Green Fund (in which IFC is a cornerstone investor) and a separate $9 million debt facility from the DFC.

Three companies. Three continents of DFI money. One structural question worth answering: why e-mobility, and why now?

THE ASSET THAT CHANGED THE CALCULATION

The honest answer is that African e-mobility operators have something that most African fintechs, most African SaaS companies, and most African platforms never had: a real, physical, recoverable asset.

A battery swap station is collateral. A fleet of 80,000 electric motorcycles Spiro's current deployed base is collateral. A bus financed under a lease-to-own arrangement, generating daily fare revenue, is collateral. These assets can be repossessed, redeployed, and sold. They do not disappear when a startup pivots or its unit economics break down.

This matters enormously to how DFIs write debt. Development banks are not venture capitalists. They do not price for a 10x exit. They price for repayment, and repayment requires an asset coverage ratio that makes sense. For the better part of a decade, African digital startups could not offer them that. The pure-play fintech a mobile wallet, a micro-lending app, a payments API carries no recoverable asset base. Its collateral is its data, its customer relationships, its growth rate. DFIs were forced to play those rounds as equity, with all the patience and uncertainty that implies.

The EV operator is structurally different. The battery a lithium-ion cell that costs between $800 and $1,200 to replace is a depreciating but recoverable asset. The swap frequency data generated by a network of 2,500 stations is underwriting infrastructure. The fleet revenue stream fares, swap fees, financing margins is a repayment schedule. When Afreximbank extended $75 million to Spiro, it was not making a bet on disruption. It was making a lending decision.

This is not charity dressed as investment. It is the most coldly rational capital allocation decision in African tech right now.

THE SHIFT IN DFI BEHAVIOUR

The structural move toward debt was not spontaneous. It is measurable.

In early 2025, equity represented 76% of all capital raised by African startups. Development finance institutions were active equity participants in climate and fintech rounds Norway's Norfund, Belgium's EDFI Management Company, the UK's BII writing growth-stage equity alongside venture funds.

In the first five months of 2026, that pattern reversed. Debt capital rose from 24% to 57% of all African startup funding — a 165% increase in absolute terms. By May 2026, roughly 80% of capital raised across the continent was structured debt, not equity.

The DFIs that once took equity stakes are not gone. They are writing debt cheques instead. The implication for founders is significant: the institutions with the deepest pockets and the most patient capital are no longer available at the equity cap table. They are in the debt stack, secured against your assets, and they want repayment, not returns.

For e-mobility operators, this is a competitive advantage measured in basis points. DFI debt costs materially less than commercial bank debt in any African market. The Kenyan commercial lending rate sits above 15%. A DFI senior debt facility, structured with impact covenants and a blended finance wrapper, can price at 7–9%. For a company importing lithium-ion cells at scale, that differential in cost of capital applied to $50 million — is worth millions of dollars per year in operating margin.

The operators who are DFI-creditworthy are not just capitalized better. They are structurally cheaper to run.

WHO IS EXPOSED, AND HOW

Spiro is the clearest beneficiary of the DFI debt moment. Its capital structure is almost entirely DFI-anchored: FEDA equity, Africa Go Green Fund debt, Nithio climate debt, Impact Fund Denmark equity. Its $343 million total raise has been built, layer by layer, from the development finance system outward. That is a deliberate choice by its leadership, and it has created a cost structure that no VC-backed e-mobility competitor can replicate from a standing start.

Ampersand's DFC and Africa Go Green Fund relationships are smaller in absolute terms $16.5 million combined — but strategically significant. They establish Ampersand as DFI-creditworthy ahead of its scaling phase. The Rwanda government's parallel policy posture zero import duty on EVs, VAT waivers on locally assembled vehicles — means Ampersand is building in the one East African market where DFI debt economics and government policy are pointing in the same direction.

BasiGo carries more complexity. The Proparco equity stake and BII/DFC debt was assembled on the assumption that Kenya's 2025 EV policy framework zero-rating, import incentives, assembly support — would hold. Monday's edition covered what the Finance Bill 2026 threatens to do to that assumption. If the exemption clause survives to July 1, BasiGo faces not just higher landed costs but a question about whether the asset quality that underwrote its DFI debt still looks as clean. DFI lenders do covenant reviews. Policy reversals are exactly the kind of trigger that prompts them.

THE EAST AFRICA CONTEXT

Development finance does not flow neutrally across markets. It follows policy environments the way water follows a channel.

Rwanda has built the most DFI-receptive EV policy environment in East Africa: zero import duty, VAT waivers, a government actively courting Ampersand, BasiGo, and every battery swap operator with regional ambitions. Kigali is not trying to be the biggest EV market. It is trying to be the most DFI-legible one — and there is a difference.

Kenya was, until the Finance Bill 2026 was tabled, the most compelling combination of market scale and policy support in the region. If that bill passes, the DFI lending thesis for Kenya-based EV operators does not collapse but it requires renegotiation. Asset values fall when landed costs rise. Repayment schedules built on fleet economics absorb a 16% input VAT reclassification as a direct hit to free cash flow.

Tanzania is further behind on both counts but watching closely. The WAGA Motion EV roadmap is being built in a market where the policy environment is neutral rather than actively hostile. Neutral is not a competitive disadvantage when the alternative is volatile.

THE CHARGED READ

There is a version of the DFI debt story that sounds like good news for African e-mobility and nothing else. But the structural shift matters for every African founder operating in capital-intensive sectors.

The era of DFI equity where development banks took growth-stage equity alongside VC, providing patient capital with little pressure for near-term returns is over for now. What replaced it is a more demanding regime: DFI as creditor, secured against real assets, with covenants, repayment schedules, and the full weight of institutional oversight.

That is not bad news for well-run operators with real assets and real revenue. It is a filter. The companies that survive it will be the ones that built for debt serviceability alongside growth not just the ones that could tell the best story in a pitch room.

Having sat across the table from banks trying to underwrite informal SMEs at Ramani, I can tell you that the asset quality conversation is not abstract. The question a DFI lender asks an EV operator is the same question a commercial lender asks a leasing company: when the borrower cannot pay, what do we have? The EV sector's answer batteries, stations, fleet assets is now good enough to unlock $300 million in eighteen months.

That is not a narrative. That is a balance sheet.

The next phase of African e-mobility will not be decided by who raises the most venture capital. It will be decided by who becomes, and stays, DFI-creditworthy.

CHARGED is published every Monday (The Week in Numbers) and Thursday (Deep Signal). Dar es Salaam.