THE COLLATERAL QUESTION

Capital is not just rotating between sectors. It is applying a filter — and most African fintechs don't pass it.

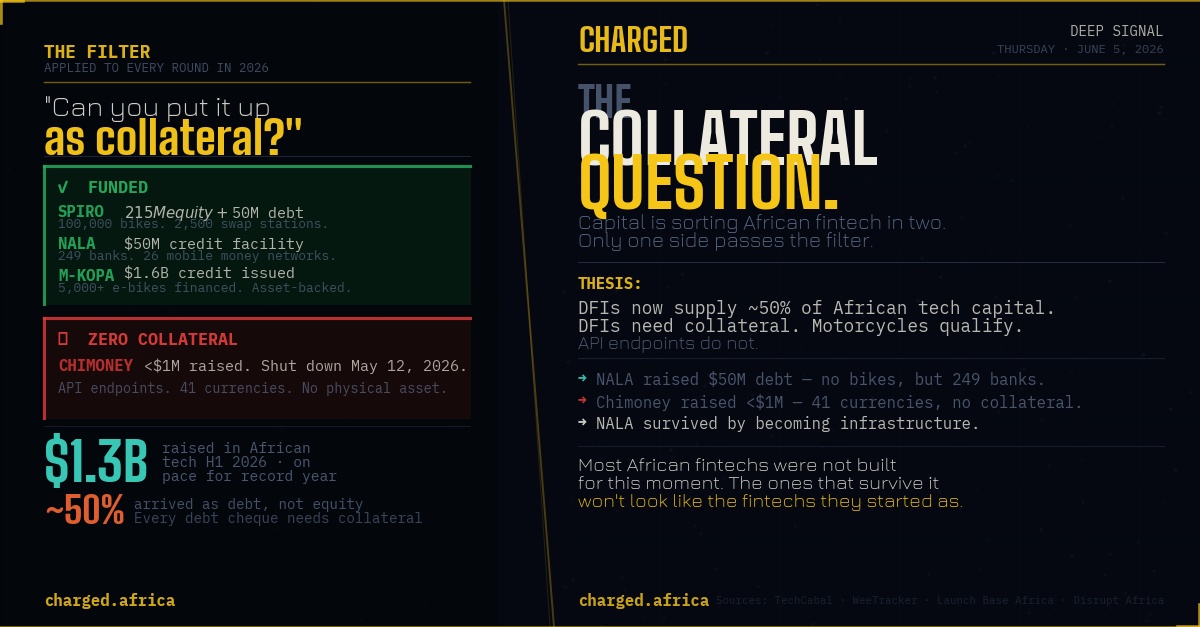

On Monday, CHARGED ran the data: $575M in 60 days, 83 companies funded, Spiro's $215M equity round. The headline told you what happened. Today I want to tell you why — because understanding the mechanism is what separates operators who are going to raise their next round from those who are already running out of road.

The thesis: African fintech is being sorted, right now, by a single question that most founders never thought would matter. Can you put it up as collateral?

That question is reshaping the continent's entire capital stack.

THE FILTER NOBODY POSTED ABOUT

When Afreximbank writes a $50 million debt cheque, it needs an asset on the other side of the ledger. When IFC structures a mezzanine facility for an energy company, it is running a DCF model on physical infrastructure — cables, meters, solar panels — not a dashboard showing DAU and cohort retention.

This is not a new insight about development finance. What is new is the scale and speed at which DFIs have become the dominant capital source for African tech in 2026. Africa's startup ecosystem has now raised $1.3 billion in H1 2026, on pace to break the full-year record. But look at the instrument composition: an estimated 50% of that capital has arrived as debt, not equity. That is structural, not cyclical.

Debt capital needs collateral. And the only African tech companies that pass the collateral test are the ones that have buried their fintech inside something physical — a motorcycle, a battery, a swap station, a solar panel, a bus.

This is the rotation. Not sector rotation. Instrument rotation. And it is quietly deciding which companies get funded and which ones do not.

THE TWO FINTECHS

There are now two kinds of fintech operating in Africa, and they are drifting further apart every quarter.

The first kind looks like what you'd expect: a mobile app, a payment API, a cross-border remittance engine, a B2B SaaS layer for banks. Built light. Scalable. Capital-efficient until it isn't. This is the fintech that raised well in 2021 and 2022 on equity from global VCs who believed the infrastructure story. Chimoney was this fintech. Its cross-border payment product worked. Uchi Uchibeke built something technically sound. It raised under $1 million across four years and shut down on May 12.

The second kind has a different architecture. Its product is still software — credit scoring, payment rails, fleet management — but the delivery mechanism is physical. The customer acquisition channel is a motorcycle or an e-bus. The repayment infrastructure is a battery swap. The credit underwriting model is 30 million transaction data points generated by 100,000 riders over three years of daily operations. This is Spiro. This is M-KOPA. This is Watu Africa, generating $37M in quarterly profit with 40% of its loan book tied to EV asset financing.

One of these fintechs can take a $50M debt facility. The other cannot. That is the filter.

THE EXCEPTION THAT PROVES THE RULE

Two days ago, NALA — founded here in Tanzania, four YC rejections and a government shutdown behind it — announced a $50 million credit facility from Mars Growth Capital, a joint venture between Liquidity and Japan's MUFG Bank. NALA builds stablecoin payment rails and cross-border infrastructure. It does not have a motorcycle. It does not have a battery swap station.

So how did a pure-play fintech raise $50 million in debt in this environment?

Look at how NALA is built. It is not a consumer remittance app. It is infrastructure for 249 banks and 26 mobile money services across 16 countries. Its enterprise platform, Rafiki, moves money through institutional corridors — settlement rails that touch real balance sheets, real banks, real mobile money operators. NALA's collateral is not a physical asset. But its clients are institutional. Their transaction volumes, their regulatory relationships, their guaranteed payment flows — that is the asset on the other side of the MUFG ledger.

NALA survived the collateral test not by having motorcycles, but by becoming infrastructure that institutions depend on. The lesson is not that you need hardware. The lesson is that you need something a DFI can underwrite a real asset, a real institution, a real claim on future cash flows. Developer dashboards and API endpoints don't qualify.

WHAT SPIRO'S NEXT MOVE SIGNALS

The $215M announcement included details that most coverage glossed over. Spiro is not just expanding to Ethiopia and the DRC. It acquired a UK engineering firm last month to build an R&D centre in Nairobi. It is building solar-powered swap stations and battery storage systems alongside its expansion.

Think about what those moves communicate to the next capital allocator looking at the deal: Spiro is deepening its physical footprint, not reducing it. Every solar panel, every swap station, every manufacturing facility in Kenya, Rwanda, and Uganda is another asset on the balance sheet, another line of collateral, another reason a DFI can justify a $100M debt facility in 2027.

The Nairobi R&D centre is the tell. The company that already dominates Africa's two-wheel EV market with 100,000 motorcycles is now investing in the intellectual property to manufacture and improve the hardware itself. It is closing the loop from operator to OEM. At that point, Spiro's cap structure conversation stops being about the next fundraise and starts being about whether it prices an IPO or entertains a strategic acquisition from a global mobility player.

This is not where most African tech companies aspire to be. It is where the rotation is heading.

IMPLICATIONS

For operators: If your business cannot answer the question "what can I put up as collateral?" — start building the answer now. That does not necessarily mean hardware. It means institutional revenue, enterprise contracts, regulated assets, or a data moat so proprietary that it becomes an underwritable claim. NALA found one path. Spiro found another. Both are getting funded.

For capital allocators: The equity returns in African tech for the next cycle are most likely going to come from the companies that successfully navigate from DFI-debt-fundable to IPO-or-strategic-acquisition. Watch the ones that are building manufacturing capacity, proprietary data infrastructure, and institutional client bases simultaneously not the ones still trying to win on margin by building cheaper payment APIs.

For everyone: LemFi just took a strategic investment from Tether to integrate USDT as its settlement layer. Cross-border remittances are moving from SWIFT to stablecoin rails. That transition will produce new infrastructure winners but only the ones that can plug into institutional balance sheets on both ends of the corridor.

The collateral question is not going away. The capital that answers it is already moving.

THE CHARGED READ

I have spent time on both sides of this rotation —sitting across the table from DFI investment officers trying to structure debt for asset-light companies, and building the case for fleet-based financing models that work precisely because the motorcycle is the collateral. The structural logic is not complicated. What is complicated is building a company that passes the test.

Most African fintechs were not built for this moment. The ones that survive it will not look like the fintechs they started as.

The rotation is not just about where capital flows. It is about what survives.