Two Wheels. $150 Million. One Grid.

The real Africa EV story isn't about electric cars. It's about 30 million motorcycles, battery-as-a-service, and the financing model that's making it all click.

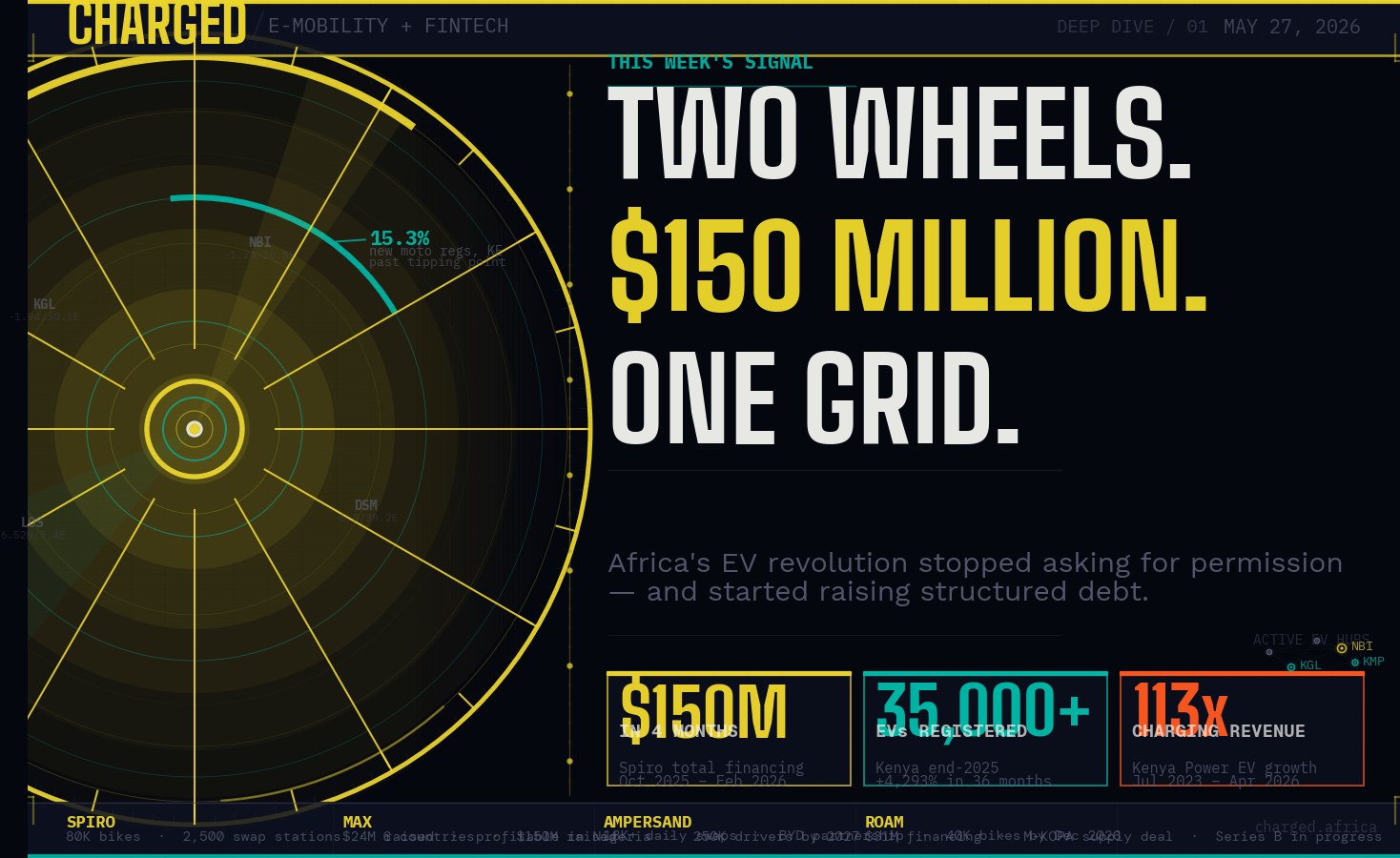

Kenya ended 2025 with more than 35,000 registered electric vehicles — up from just 796 three years earlier. That's a 4,293% increase in 36 months. But the more precise signal is this: electric two-wheelers now account for 15.3% of new motorcycle registrations in the country, crossing the 5% adoption threshold that technology economists treat as the tipping point. Past that line, historically, consumer tech transitions have been irreversible.

Then there's the Kenya Power number that should be in every investor deck but isn't. Published quietly this month: the national utility earned KES 382 million (~$2.9 million) from EV charging over 34 months — with monthly revenue from charging growing 113-fold between July 2023 and April 2026. The boda boda rider in Kisumu is now a revenue line in a national utility's quarterly report.

This is no longer early-stage. This is infrastructure.

The Race That Isn't About Vehicles

Africa's EV conversation has spent too long in the wrong frame. The question was never will Africa go electric? That debate closed quietly sometime around 2024 when institutional debt — not venture capital — started flowing into two-wheel mobility companies. The question now is who controls the infrastructure layer, and whether the companies building it are African or not.

The answer is clarifying fast.

In early 2026 alone, African e-mobility startups secured over $75 million in financing — led by Spiro's $50 million debt facility and MAX's $24 million equity-and-debt round. These aren't seed cheques. They're the kind of structured, asset-backed financing that implies operational maturity: recurring revenue, collateralizable assets, and data that lenders can actually underwrite.

The instrument is the signal.

The Business Model That Looks Like Fintech

Here is the part that should interest everyone who reads CHARGED for the fintech half: the model making EV scale possible across Africa is not a vehicle business. It is a financial services business wearing a motorbike.

Battery-as-a-Service (BaaS) is the mechanism. Instead of buying a $1,300–$1,500 petrol motorcycle, a rider pays roughly $800 upfront for an electric motorcycle — then pays a daily or per-swap fee for battery access. The battery stays off the rider's balance sheet. The operator owns the energy asset and earns recurring revenue per swap. It is the same structural logic as M-KOPA's asset financing model: own the asset, monetize it over time, use behavioural data to manage credit risk.

This is why the capital flowing into African EV is debt, not equity. The swap station is the collateral. The swap transaction history is the credit data. The rider's daily earnings are the repayment source.

Having sat on both sides of this equation — underwriting informal SMEs at Ramani and building an EV roadmap at WAGA Motion — I can tell you: the unlock here isn't the battery chemistry. It is the ability to instrument rider behaviour well enough to price risk. When you know how many swaps a rider does per day, which routes they ride, and what their average earnings look like, you can lend against that. That is what makes the unit economics work. That is what makes this a fintech story as much as a mobility story.

The Companies Setting the Pace

Spiro is the continent's largest e-mobility operator — 80,000 electric motorcycles, 2,500 battery swap stations, and over 30 million completed swaps across six countries: Kenya, Uganda, Rwanda, Nigeria, Benin, and Togo. Their $150 million in financing over four months signals something structural: Afreximbank and institutional lenders now view battery-swap infrastructure the same way they view telecom towers — recurring-revenue, asset-backed, worth financing at scale. Pilots are underway in Cameroon and Tanzania.

MAX (Nigeria, founded 2015) is the fintech play made explicit. The company raised $24 million in January 2026 after hitting profitability in Nigeria — a milestone that reframed the narrative from "mobility startup" to "operational business." Their pitch isn't the motorcycle. It's the fleet management software, the IoT data layer, and the PAYG financing platform for commercial drivers. They are underwriting riders the way lenders underwrite borrowers: transaction history as credit proxy. Target: 250,000 drivers and $150 million in annual recurring revenue by 2027.

Ampersand (Rwanda and Kenya, founded 2016) is the East African precision play. Currently operating 5,800 electric motorcycles with 18,000+ battery swaps daily, they raised $7 million in August 2025 and announced a partnership with Chinese manufacturer BYD to produce 40,000 electric motorcycles in Rwanda and Kenya by end of 2026. Their 2030 vision: 600,000 motorcycles across East Africa — a fleet that would make them the continent's largest EV operator by units deployed.

ROAM (Kenya, founded 2017) is the manufacturer betting that local production is a moat, not just a story. With $31 million in total financing, a 10,000 sqm assembly plant in Nairobi, and a Series B targeting $15–20 million, ROAM's supply agreement with M-KOPA — Africa's largest asset-based fintech — is the cleanest proof of concept in the market. Riders finance ROAM bikes through M-KOPA's platform. EV hardware meets fintech distribution. The model the industry has theorised about for years is already operating in Nairobi.

What East Africa Got Right (And the Rest of the Continent Is Still Working Out)

The East African lead isn't luck. Three conditions converged:

Motorcycle taxi density. Kenya alone has approximately 3 million boda boda riders supporting 5 million livelihoods. These riders operate 8–12 hours daily and have every rational incentive to cut fuel costs. When an electric motorcycle saves a rider $3–5 per day in fuel versus a petrol bike, the value proposition is not theoretical. It shows up in weekly net income.

Grid stability. Unlike West African markets where load shedding forces operators onto expensive solar-powered off-grid infrastructure, Kenya and Rwanda have relatively reliable electricity access. Ampersand's swap model depends on the grid being on. Kenya Power's $2.9 million in EV charging revenue over 34 months is the empirical proof that reliable charging demand exists.

Regulatory momentum. Kenya launched its National Electric Mobility Policy in February 2026. Tanzania is developing its own EV roadmap. These are not just policy documents — they are long-term signals to capital that governments are making durable bets. For investors doing multi-year debt structures, that signal matters enormously.

The constraints are real, though. In markets with unreliable grids, the BaaS model requires costly solar integration that changes the economics. High import duties in several markets still add 20–30% to EV hardware costs, absorbing the fuel savings that are supposed to be the value proposition for riders. And every major operator is running proprietary battery ecosystems — meaning Spiro's batteries don't work in Ampersand's stations, and vice versa.

That last point is the industry's self-inflicted wound.

Three Things to Watch in the Next 18 Months

Battery standardisation. If Africa ends up with four incompatible swap ecosystems, the continent gets a VHS/Betamax situation — fragmented infrastructure that slows adoption, raises switching costs, and hands the advantage to whoever can consolidate. An open-standard battery consortium for African e-mobility is the unlock no single operator wants to propose first. Watch for who blinks.

Gotion's gigafactory. Chinese manufacturer Gotion High-Tech is building Africa's first battery gigafactory a $5.6 billion project targeting 20 gigawatt-hours of annual output, scheduled to begin production in 2026. If it delivers, it fundamentally changes the cost curve for every operator importing batteries from Asia. If it stalls, African operators remain dependent on the supply chains that are already under tariff pressure globally.

The Tanzania signal. East Africa's missing piece. Kenya has the policy, the registrations, and the charging revenue. Tanzania has the boda boda density, the corridor links to Rwanda and Uganda, and — at WAGA Motion — an EV roadmap being built with serious intent. Whoever cracks Dar es Salaam cracks the growth axis of the entire region. The capital is watching.

The boda boda rider in Kisumu doesn't think of himself as a proof of concept. He just knows his fuel bill dropped, his daily income went up, and the swap station charges his battery faster than he can eat lunch. That's the adoption story no external analyst would have written for Africa. But Africa didn't wait for permission to write it.

Thirty million motorcycles. One switching moment. The infrastructure layer is being built — and the question is who owns it.

CHARGED Newsletter — May 27, 2026 Deep Dive: E-Mobility + Fintech Intersection | Geographic focus: East Africa + Pan-African Primary sources: Kenya Power, Africa: The Big Deal, TechCabal Insights, CleanTechnica, Semafor, EV24.Africa