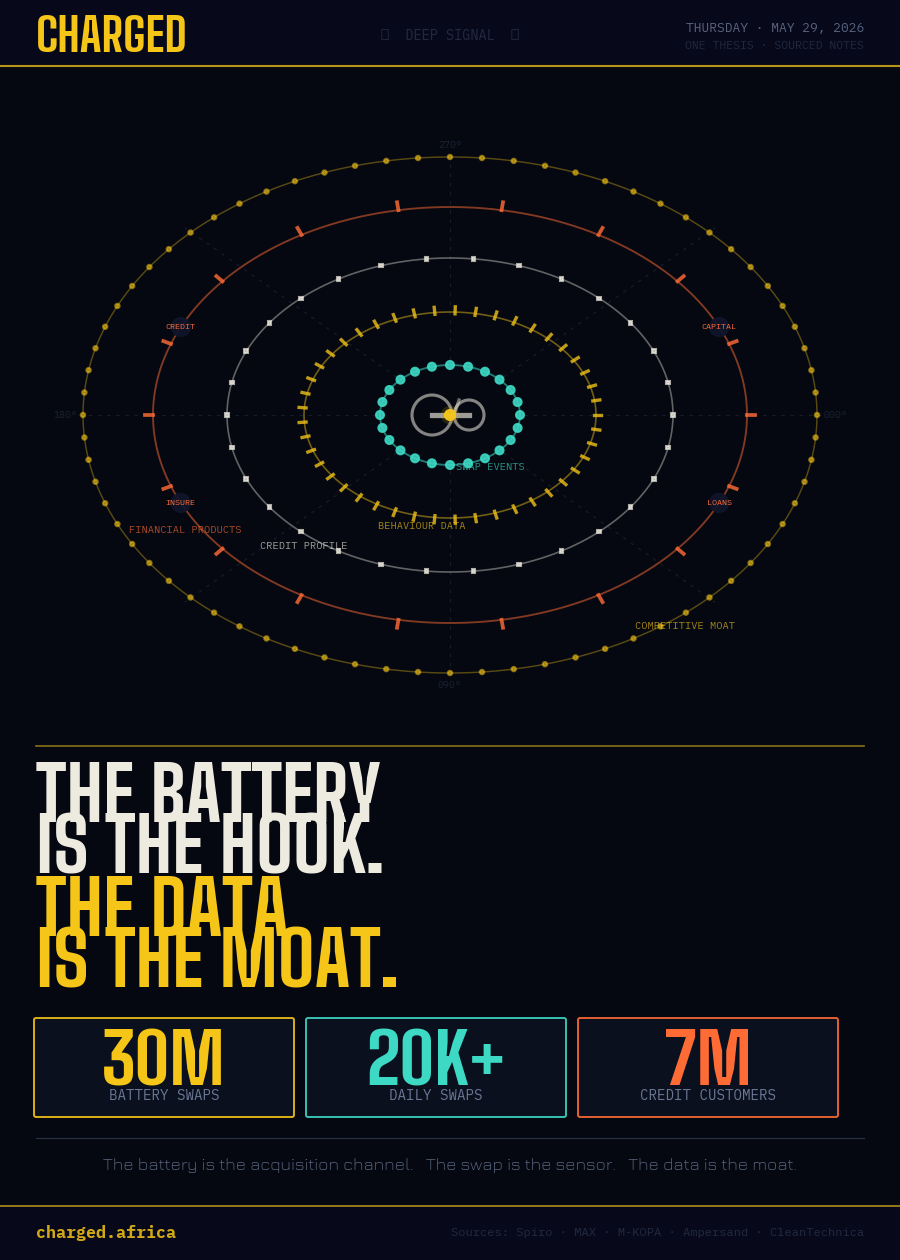

1. Spiro has completed 30 million battery swaps across six countries.

Thirty million discrete transaction events, each carrying timestamp, location, battery state, rider ID, and swap frequency. Spiro operates 2,500+ swap stations and 80,000 motorcycles across Kenya, Uganda, Rwanda, Nigeria, Benin, and Togo. Most analysts cite the station count as the moat. The station count is not the moat. The transaction log is. Source: Spiro February 2026 funding announcement / CleanTechnica

2. MAX uses IoT sensors to monitor rider behaviour in real-time and uses that data to underwrite credit.

Every MAX motorcycle is instrumented: vehicle health, payment consistency, route patterns, usage hours. The company's proprietary fleet management system uses that data to predict default risk before it materialises. Riders who demonstrate consistent repayment behaviour build a digital credit profile that unlocks additional financing on the next bike, on working capital, on insurance. MAX raised a further $8M in debt from Triple Jump in May 2026, specifically to scale this asset-backed lending model across West Africa. Source: MAX, Launch Base Africa, TechNext24 May 2026

3. M-KOPA has disbursed over $2 billion to 7 million customers using daily payment data as the primary credit signal.

M-KOPA finances electric motorcycles with deposits as low as KES 10,000 and daily repayments of KES 450–527. Each daily payment is a data point. Enough data points, and a rider's credit identity is established — unlocking digital loans, health insurance, and further asset financing. M-KOPA has financed over 5,000 electric motorcycles in Kenya. Bolt onboarded more than 1,700 M-KOPA-financed riders, hitting its 2025 target ahead of schedule. The flywheel from transport payment to financial product is already spinning. Source: M-KOPA Newsroom, Semafor, WeeTracker — 2025/2026

4. Ampersand is making a deliberate strategic bet: become the infrastructure, not just the operator.

In December 2025, Ampersand opened its battery swap network to third-party electric motorcycle manufacturers the first open swap network for third-party bikes in Africa. This looks like generosity. It is not. Every third-party bike that plugs into Ampersand's network generates another stream of swap transaction data. Ampersand is trading exclusivity for dataset breadth. At 20,000+ daily swaps across Rwanda and Kenya, they are building the richest behavioural dataset in East African e-mobility regardless of which brand the rider is sitting on. Source: CleanTechnica, Africa Sustainability Matters December 2025

5. The credit moat compounds — and the window to build it is narrowing.

M-KOPA's model did not become defensible because of its technology. It became defensible because of its 18 months of daily payment history on millions of customers — data that took years to accumulate and is impossible to replicate instantly. E-mobility operators building transaction histories today are building the same compounding advantage. Operators who delay — who treat data as a byproduct rather than a strategic asset — will find themselves trying to catch up against incumbents whose credit models are already calibrated on three years of rider behaviour.

THE COUNTERARGUMENT

Data moats are only moats if riders stay within one network. If battery standardisation advances — and there are real efforts to establish open standards across African e-mobility operators — a rider could freely switch between Spiro, Ampersand, and any new entrant with a compatible battery. Fragmented swap histories mean fragmented credit profiles. The moat dissolves.

This risk is real, but it cuts both ways: it is exactly why operators should be racing to lock in transaction depth before standardisation forces openness. The operator with the longest and richest transaction history per rider will still have the most accurate credit model, even in an open-standard world. Recency does not substitute for depth. A new entrant in 2028 will not be able to buy three years of rider data.

IMPLICATIONS FOR OPERATORS

Build the data infrastructure before you think you need it. The temptation is to treat IoT, fleet telemetry, and payment tracking as operational tools. They are not. They are the primary long-term asset of the business. Instrument every bike, every swap, every payment, every route — now, while the dataset is still young enough to be worth building.

Credit product expansion is not a "later" decision. M-KOPA's path — daily transport payments unlocking loans, then insurance, then merchant credit — is a roadmap, not a coincidence. The operators who wait until they feel "ready" to launch financial products will find that a fintech with a partnership deal got there first. Define your credit product roadmap in the next twelve months, not the next five years.

Network openness is a data strategy, not just a partnership strategy. Ampersand's decision to open its swap network to third-party manufacturers deserves a close reading. The question every operator should ask is: does keeping our network closed give us a bigger data advantage, or does it just give us a smaller network? In most markets, the answer is the latter.

The swap station is a branch. Every battery swap station is a daily touchpoint with a rider. It knows when they arrive, how depleted their battery is, and how frequently they return. Operators who treat swap stations as purely logistical infrastructure are leaving the most valuable layer of the asset unmonetised.

IMPLICATIONS FOR CAPITAL ALLOCATORS

Underwrite the data layer, not just the asset base. When evaluating an e-mobility operator, the standard checklist — fleet size, station count, revenue, unit economics — is necessary but insufficient. Add a data audit: How many transaction records do they have? How long is their rider history? How is the data structured, and is it being used for credit decisioning? The answers determine how defensible the business is in year five, not year one.

Transaction history depth should inform debt sizing and tenor. An operator with 24 months of rider payment data on 10,000 bikes has demonstrated default rates that a lender can actually underwrite. An operator with six months of data on the same fleet is a different risk profile entirely. Debt facilities should reflect this distinction explicitly and the best operators should be demanding it as a differentiator.

Watch for the fintech pivot signal. When an e-mobility operator starts announcing insurance products, digital lending, or merchant credit lines that is the signal that they have cracked the data layer and are beginning to monetise it. This is a leading indicator of durable margin expansion, not a distraction from the core business. Ampersand and MAX are both moving in this direction. Capital that understands this is positioned early. Capital that misreads it as "mission creep" will be slow.

The M-KOPA parallel should anchor your valuation framework. M-KOPA reached 7 million customers and $2 billion in disbursements primarily through disciplined accumulation and use of daily payment data. E-mobility operators with comparable data ambitions and comparable transaction depth deserve comparable capital structures. The comparison is not perfect, but it is more useful than comparing them to hardware companies.

THE SIGNAL

In five years, the most valuable thing Spiro owns will not be its 2,500 swap stations.

It will be its 30 million transaction records.

CHARGED Deep Signal is published every Thursday one thesis, sourced, with implications for the operators and allocators building the next layer of African infrastructure